The latest news from the housing sector continues to be bad. Home prices declined sharply in October.

The non-seasonally-adjusted S&P/Case-Shiller 20-city composite home-price index fell 1.3% on a monthly basis and 0.8% on an annual basis in October.

Prices hadn’t dropped on an annual basis since January and are 29.6% below their 2006 peak.

Six cities — Atlanta, Charlotte, Miami, Portland, Seattle and Tampa — hit their lowest levels since home prices started to fall in 2006 and 2007.

The Case-Shiller report is based on prices over a three-month period, so this report included prices from August, September and October. That makes it more accurate in revealing trends than a single month report.

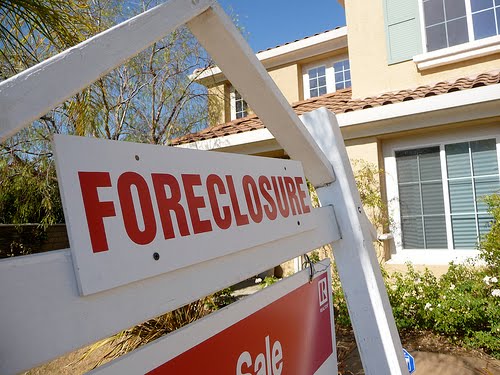

According to Bank of America Merrill Lynch, there’s an inventory of 7.2 million homes, or roughly 21 months of supply, nationwide. That includes homes that are in, or close to, foreclosure.

Think about that; there's nearly a two-year supply of foreclosures either on the market or headed to market. What will that do to home prices? Imagine what this portends for stable owners seeking to sell their homes? There's a lot of competition from very cheap foreclosures out there.

And then consider the fact that banks are holding onto foreclosed properties without listing them for sale. They're doing this with the hope that these homes will recover their lost value. The banks are hoping to at least break even, if not make a profit.

They may be waiting for years.

If banks were required to report the true value of the homes on their books, and thereby report their true losses, many more of them would be insolvent. As it stands, 157 US banks have already gone under in 2010. But even some of the biggest banks, the Mega Banks, are on very shaky ground.

The price declines will inevitably push even more mortgages underwater. At present, nearly a quarter of all homes with a mortgage already have a lesser value than they are mortgaged for. That number will only increase.

The process of price discovery, which is necessary to determine the final value of housing, is still years away. Prices will continue to fall in 2011 and in 2012.

That's because there's still the problem of option-ARM loans that will reset over the next two years. Option ARMs — which became widespread in 2005 — let borrowers choose to make very low payments for the first five years.

During that initial period, borrowers were allowed to pick their payment option, including just the interest. According to Fitch Ratings, 94 percent of option ARM borrowers elected to make minimum payments only.

The bulk of option ARMs reset dates are spread out from 2010 through 2012, meaning the foreclosure waves will drag on for at least the next two years. That has federal and state officials bracing themselves for the next tidal wave of foreclosures

Almost all the homes with mortgages have already lost value, thereby lowering the homeowner's equity. Most of them will have a difficult time refinancing as a result.

The artificially low interest rates set by the Fed are still masking true home values. Easy money is still providing at least some incentive to buy, yet even that cannot thwart the brutal combination of price declines and falling demand.

Eventually, home prices will fall back to levels not seen since the 1990s, the 1980s, and perhaps even the 1970s in some areas.

Millions of prospective buyers are currently sitting on the sidelines, believing that the bottom has not yet been touched. They may be left waiting for a while. And the longer they wait, the longer it will take to see any meaningful sort of recovery.

At best, it is probably still years away.

No comments:

Post a Comment